COMMENTARY

Take up in the core West End markets has remained below trend in the first six months of 2023, following the strong levels of activity that were seen in the previous 12 months. Overall activity was 513,500 sq ft in Q2 bringing the year to date figure to 1.15m sq ft in 347 transactions.

Pre lets continued to dominate activity, with the largest letting in Q2 being the 88,327 sq ft pre let to Chanel at BEAM’s new development at 38 Berkeley Square, with the building expected to be ready for occupation in mid 2024. The other major pre let was at LandSec’s the Lucent on Sherwood Street, where a confidential letting of 49,385 sq ft to a financial services group completed.

Demand remained strong but has slipped back slightly from levels seen at the end of the first quarter, falling to 5.21m sq ft from 5.61m sq ft in Q1. Requirements in most size bands have eased, although there has been a continued strengthening of demand for larger buildings (>20,000 sq ft), where demand is up by almost 800,000 sq ft (68%) since the end of last year. The creative and financial sectors remain the two most significant business groups in terms of floor space demanded but demand from the Business Services sector has strengthened significantly over the past three-six months.

Prime rents in St James’s moved to a new peak of £140.00 per sq ft and prime values in Marylebone and Fitzrovia achieved new peak rental levels of £100.00 per sq ft and £95.00 per sq ft respectively in Q1. Prime rents across the core West End markets have increased by 8.3% on average over the past 12 months.

Supply across the core West End market has increased by 225,000 sq ft in Q2, prompted by the completion of several new schemes and the release of space back onto the market as some occupiers look to take advantage of releasing space in the light of the strong growth in rents. Grade A supply moved to 1.4m sq ft, with a number of larger spaces being launched or coming back to the market, most notably at The Post Building, where Nationwide are marketing 88,680 sq ft of space, although 50% of the space was under offer at the end of Q2. The availability rate remains below the long run average (6.0%) at 5.2%.

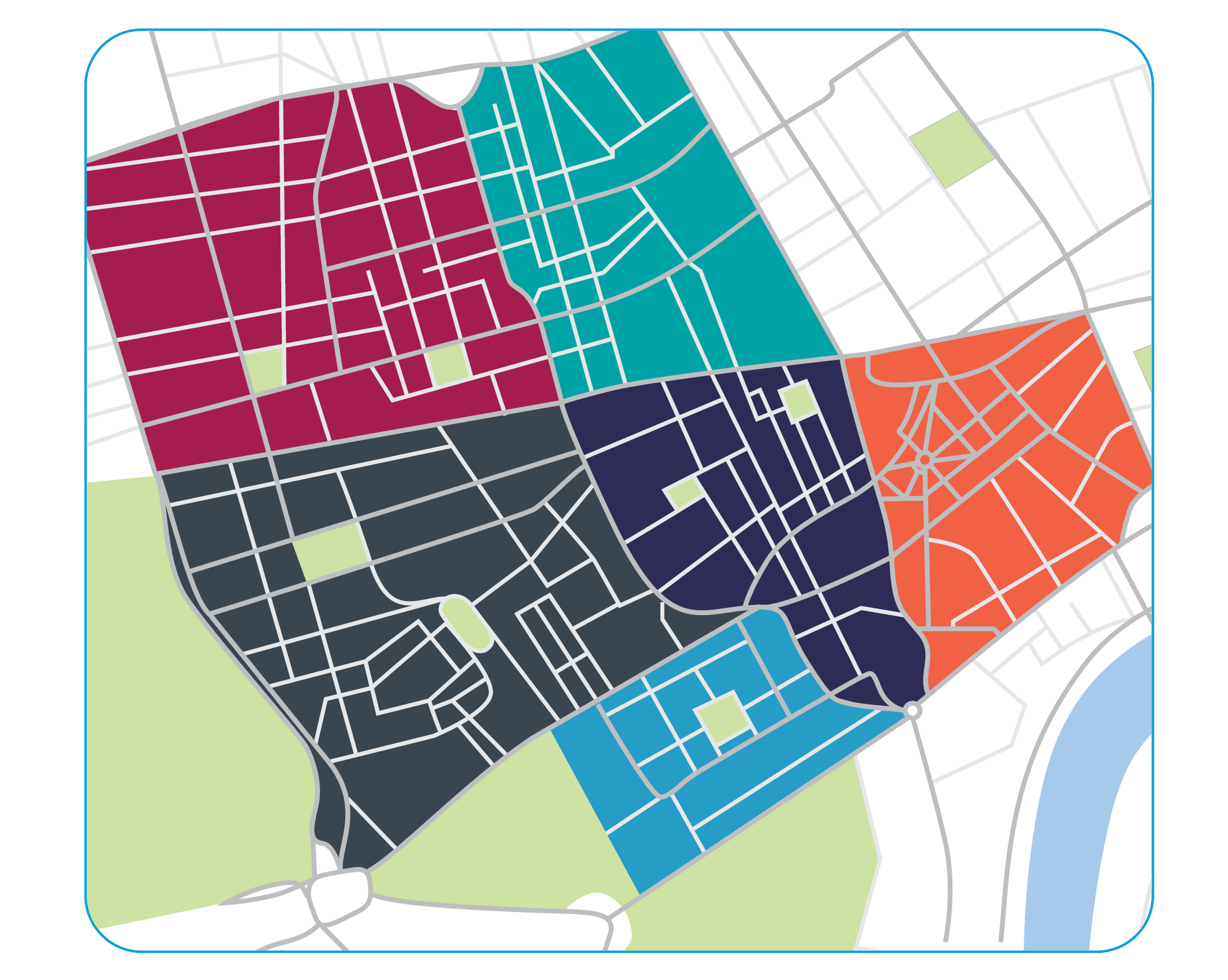

MAYFAIR OFFICE MARKET

COMMENTARY

Take up has continued to exceed trend levels in the Mayfair market, totalling 372,350 sq ft in 86 lettings the first six months of the year. Activity has been relatively evenly spread in the first two quarters, with 182,100 sq ft of transactions completing in Q2, compared to 190,250 sq ft in Q1.

The largest letting in the year to date is Chanel’s pre let of BEAM’s new development at 38 Berkeley Square, where the fashion group took the entire building of 88,327 sq ft for its global headquarters. The move more than doubles Chanel’s current floor space and signifies the company’s continued commitment to the London market. The development is the first new building to be constructed on Berkeley Square for 20 years and is expected to be ready for occupation in mid 2024.

Rents remained stable in the Mayfair market in Q2 2023, with prime rents having returned to their 2015 peak of £135.00 per sq ft. Rents on Grade B and Grade C space have now moved to new peak levels for the Grade of property, standing at £92.50 per sq ft and £69.50 per sq ft respectively.

Availability continued to edge up in Q2, rising to 591,100 sq ft at the end of June 2023 and is now 17% above the level seen at the start of the year. The main increase in availability has arisen through the increase in Grade A space, with a number of new refurbishments adding to the overall quality of stock on the market. Grade A space now accounts for 55% of all stock on the market in Mayfair.

ST JAMES’S OFFICE MARKET

COMMENTARY

Take up in the St James’s market eased in Q2 with a lack of supply holding back the number of transactions. Activity for the quarter totalled 31,100 sq ft bringing the year to date figure to 128,900 sq ft in 44 transactions.

The second quarter’s activity was dominated by smaller transactions to the financial services sector, with the largest deal being the 6,011 sq ft letting to Plurimi Wealth Management, which took the remaining four floors at the recently refurbished 30 St James’s Square.

Prime rents in St James’s recorded a new peak level of £140.00 per sq ft in Q2 2023 and have now grown by 16.7% over the past 12 months and 37% in two years. The growth in rents on Grade B and Grade C space has been more modest, rising by 20% to £90.00 per sq ft and 22% to £70.00 per sq ft respectively.

Supply edged up in Q2, moving above 200,000 sq ft once again to end the quarter at 200,575 sq ft. Several larger Grade A spaces came back to the market, the largest being the 60,433 sq ft at 12 St James’s Square, whilst six floors were released at Smithson Plaza totalling 21,478 sq ft. Grade A supply now accounts for 78% of all space on the market in St James’s, with the availability rate still the lowest amongst the West End sub markets at 3.6%.

MARYLEBONE OFFICE MARKET

COMMENTARY

Take up in the Marylebone market fell back in Q2, with a total of 85,160 sq ft of lettings completing in 31 transactions. This brings the level of activity in the first six months of the year to 244,130 sq ft, well above the trend level of activity for the Marylebone market.

Following the strong first quarter of the year, when the PIMCO deal at 25 Baker Street dominated activity, the second period saw a lack of larger lettings, with the largest transaction being Alberta Investment Management’s acquisition of 18,165 sq ft at BEAM’s 72 Welbeck Street.

Prime rents in Marylebone remained stable at their new level of £100 per sq ft and the location is now a core location for the financial services sector. Prime rents have increased by 11.1% over the past 12 months with rents on Grade B space also moving to a new peak level of £79.50 per sq ft. Grade C stock has seen rents move up to £67.50 per sq ft, although activity in this sector of the market restricted, with tenants targeting better quality accommodation.

Supply remained relatively stable at 419,230 sq ft although Grade A supply has been boosted in recent months by a number of new schemes completing and now accounts for 47% of the space on the market. The latest new development is Beltane and Angelo Gordon’s Marylebone Place at 1 Wyndham Street, which provides 77,200 sq ft of workspace over eight floors.

FITZROVIA OFFICE MARKET

COMMENTARY

Fitzrovia has seen modest levels of take up in the first six months of the year, with a total of 105,500 sq ft of activity recorded across 58 transactions. The second quarter of the year saw a slowing in the number of lettings and the majority of activity focused on the small suite market.

The largest transaction in the first six months of the year was the 12,000 sq ft letting to FinTech group Coremont LLP at Westbrook Partners new scheme at 60 Charlotte Street. The building is now fully let, with a mix of financial services and tech occupiers.

Prime rents in Fitzrovia moved to a new peak in Q1 (£95.00 per sq ft) and have remained at that level in the second quarter of the year. Rents on Grade B space continued to move up, rising to £75.00 per sq ft (7.9% growth over the past year) and this was followed by an increase in rents poorer quality space, which moved to £65.00 per sq ft.

The supply of floor space in the Fitzrovia market moved above 500,000 sq ft once again, moving to 541,300 sq ft at the end of Q2 2023. The Fitrovia market remains one of the best sources larger Grade A floor space, with two new developments of circa 50,000 sq ft having recently completed. The largest space is at the recently refurbished Berners & Wells building on Berners Street, which offers 56,250 sq ft over nine floors. The building is ready for occupation in Q2 2023. The availability rate remains one of the highest amongst the West End sub markets at 5.4%.

SOHO OFFICE MARKET

COMMENTARY

Soho saw one of the strongest levels of activity in Q2, with total lettings of 107, 950 sq ft in 26 transactions. This brings total take up for the first six months of the year to 173,200 sq ft in 60 deals.

The second quarter’s take up was enhanced by two pre lets at the soon to be completed Lucent 1 Sherwood Street. The 144,000 sq ft mixed use development provides 111,000 sq ft of office, 30,000 sq ft of ground floor and basement retail and 3,000 sq ft of residential space and is due to complete in Q3. The largest pre let was to a financial services company, which took 49,385 sq ft, whilst co working operator Myo took 25,064 sq ft on the lower floors.

Prime rents in Soho remained stable at £100.00 per sq ft in Q2 following the sharp upturn in the previous two years. Values have increased by 21.2% since the start of 2021 but remain below the peak of £105.00 per sq ft set in 2017. Rents on Grade B space have also strengthened, having moved to £79.50 per sq ft earlier in the year, with Grade C rents stabilising at £67.50 per sq ft.

Supply continued to move higher, rising to 449,152 sq ft at the end of Q2, and has now increased by 124,300 sq ft since the start of the year. The increase in stock on the market has been due to a release of both Grade A and Grade B space, which now account for 55% and 27% of overall supply respectively. The two largest Grade A buildings are Soho Estate’s Ilona Rose House, where 46,975 sq ft is still available, whilst 20 Air Street has seen a number of floors come back to the market and now offers 54,850 sq ft across two floors. The availability rate in Soho is up to 5.7% at the end of Q2 2023.

COVENT GARDEN OFFICE MARKET

COMMENTARY

Take up has remained below trend rates in Q2, with total lettings of 66,860 sq ft bringing the year to date level of take up to 124,000 sq ft in 35 transactions. The majority of lettings have been of smaller suites, with only one transaction above 10,000 sq ft since the start of the year.

The largest letting in the first six months of the years was to Spanish retailer Puig, which took 24,783 sq ft at Hines UK’s The Grain House on Dryden Street ahead of completion in the second half of the year.

Prime rents in Covent Garden moved back to £85.00 per sq ft at the end of Q2 2023, having set a new rental peak earlier in the year. Rents on Grade B space stabilised at £75.00 per sq ft following sharp increases in the aftermath of the pandemic, whilst Grade C space is now attracting rents of circa £62.50 per sq ft – still the best value across all West End sub markets.

Supply in Covent Garden has been slow to recover since the pandemic having peaked later than most other markets (Q4 2021). Availability plateaued in Q1 2023 at 446,420 sq ft, only 8% below peak levels. The increase in supply has been due to several new schemes completing, with Grade A space moving up to 193,050 sq ft and the most significant space being at the recently completed refurbishment of The Kodak at 65 Kingsway. The availability rate now stands at 6.2% and remains the highest amongst the West End sub markets.

Further information can be obtained by contacting a member of the office agency team.

Share this

West End Offices Sub Markets Research Q2 2021

West End Offices Sub Markets Research Q2 2022

No Comments Yet

Let us know what you think